In-depth articles and video walkthroughs on building, testing, and managing algorithmic breakout strategies with BreakoutOS.

No posts or videos matched

Try a different keyword - topics include filters, indicators, strategies, NASDAQ, gold, crypto, and more.

June 21, 2026

276 time strategy combinations mapped across ~20 years of E-mini NASDAQ 60-minute data in one click. Monday and Tuesday 10am-10pm emerged as the strongest long edge, while Thursday flipped short. Plus the robustness trap: an 8am-8pm window scored a perfect 100 but was untradable.

Read more →June 11, 2026

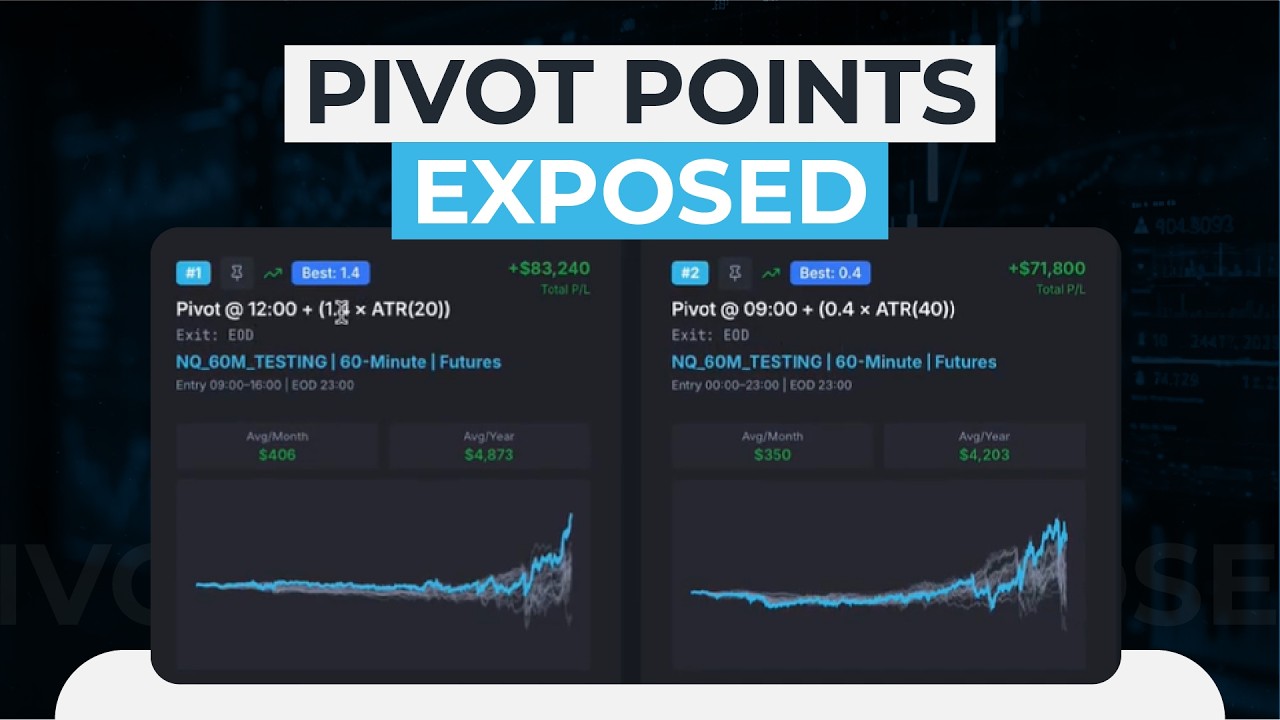

288 pivot point strategies tested on E-mini NASDAQ across 8 session boundary times and ~10,500 iterations. Midnight won on raw results, but the midday pivot won on robustness with nearly 90% of its space profitable - ATR 20, multiplier 1.4, ranked #1 in walk-forward analysis.

Read more →May 14, 2026

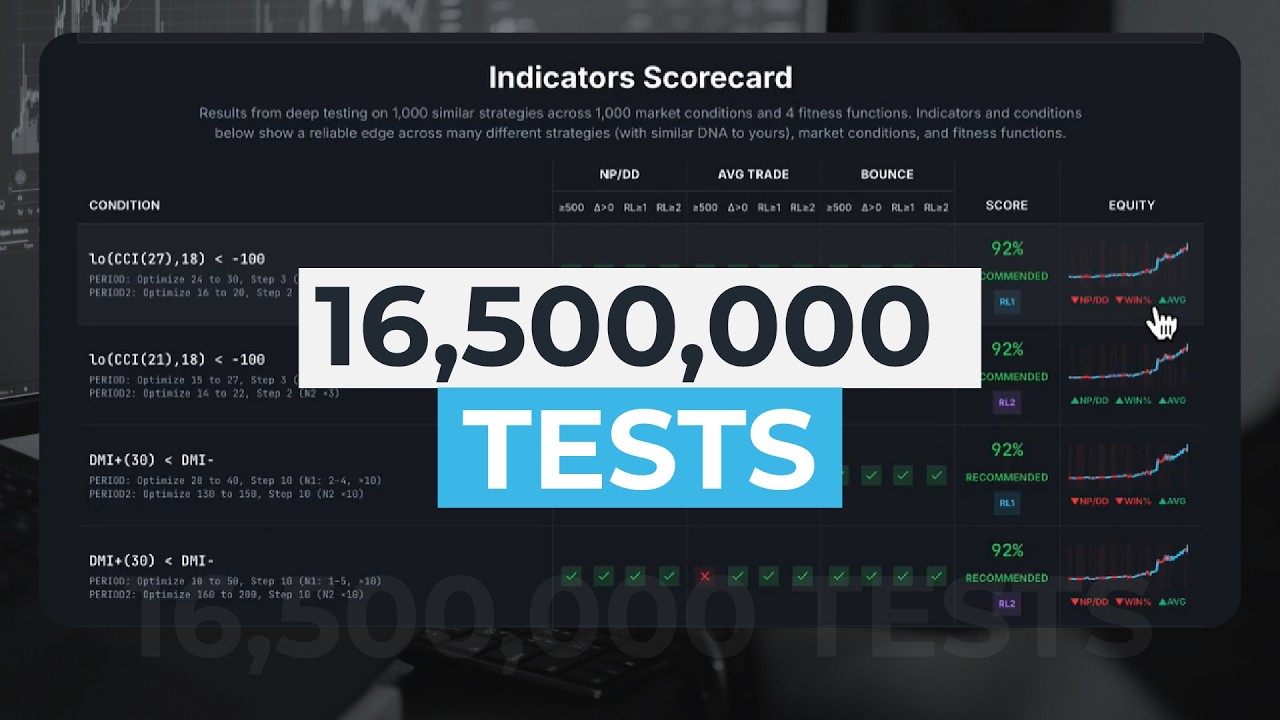

16.5 million filter tests across 1,000 NASDAQ strategies revealed a CCI-based correction filter that improved net profit on 69% of strategies and rescued 57.8% of losing variations. Here is the exact condition and why it survives unseen markets.

Read more →April 24, 2026

One condition - is the entry bar high above today's open? - cuts drawdown by 37% and improves profit-to-drawdown ratio by 53% on E-mini NASDAQ. Zero parameters, zero overfitting risk.

Read more →April 16, 2026

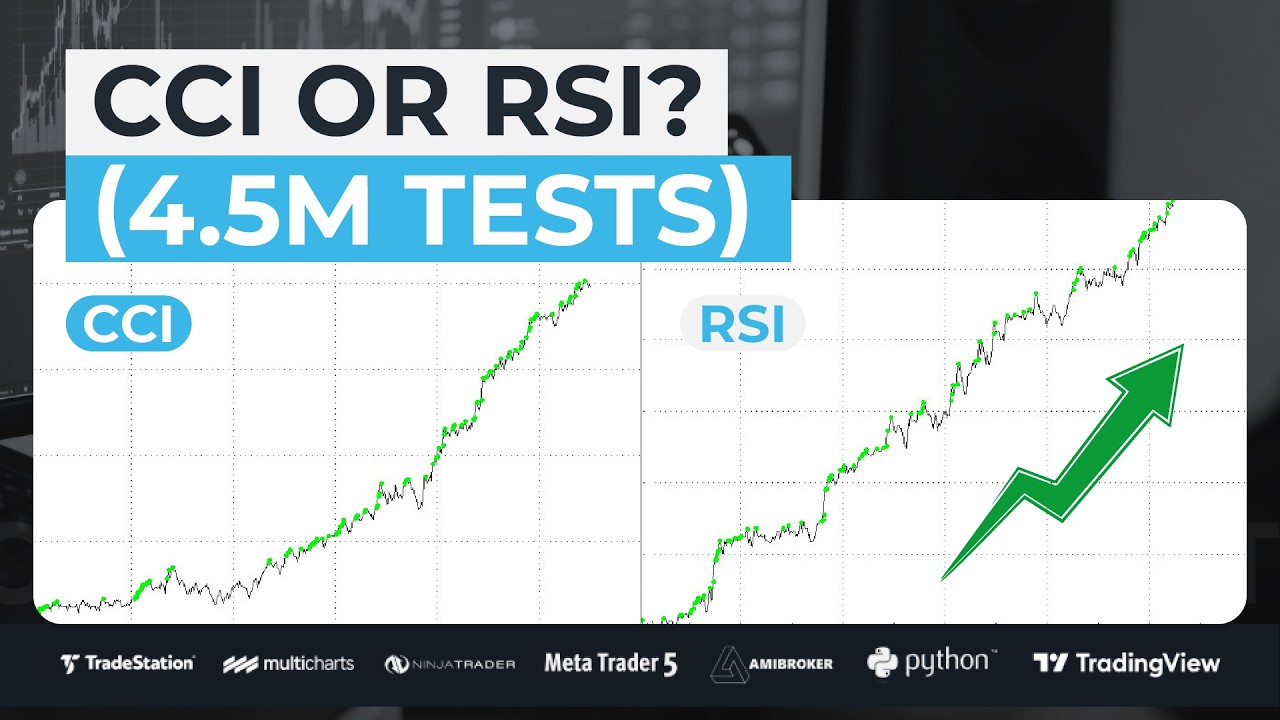

CCI improved average trade by 65% and recovered 60% of losing strategies across 4,500,000 iterations on e-mini NASDAQ. RSI's best result was 50% - barely "viable." Here is what the data shows.

Read more →April 14, 2026

SMA vs EMA tested across 1,000 strategies and 1,000 market conditions in BreakoutOS. Simple moving average improved average trade by 48% across any period. The dual EMA crossover was the top performer overall.

Read more →April 5, 2026

I tested AI across 7 real case studies: 100 AI-generated indicators, a strategy rescued with an AI filter, an ADX improved from $87K to $200K+. Here is what the data shows.

Read more →March 31, 2026

Five zero-parameter and low-parameter filtering techniques tested across NASDAQ, S&P 500, Dow, and Nikkei futures. The best technique reduced drawdowns by 79% and improved profit-to-drawdown ratio from 5 to 20.

Read more →March 27, 2026

Volatility-based indicators ranked first across both NASDAQ and Bitcoin. Oscillators ranked last. A study of 100 indicators tested on 4,100+ breakout strategies reveals which filters actually improve performance.

Read more →March 24, 2026

Win percentage has only 11% correlation between backtest and live results. Net profit has 63%. A 2,500-strategy study reveals which fitness function actually predicts forward performance.

Read more →March 20, 2026

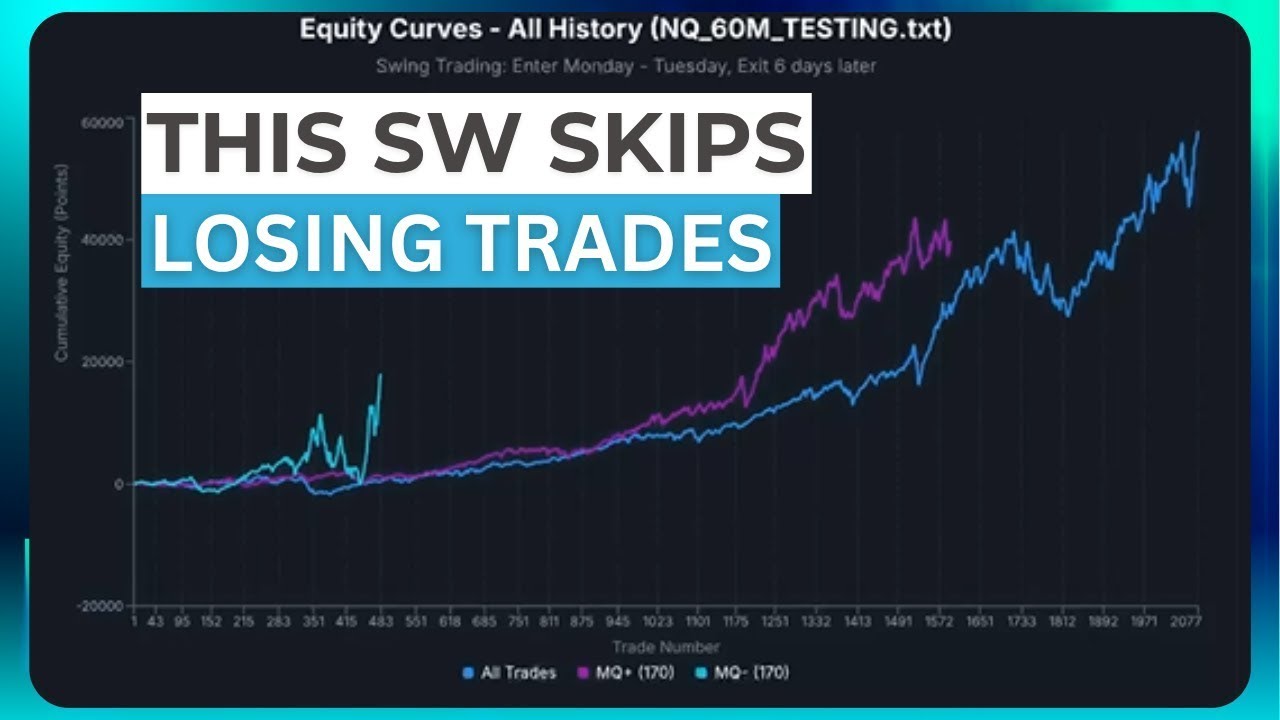

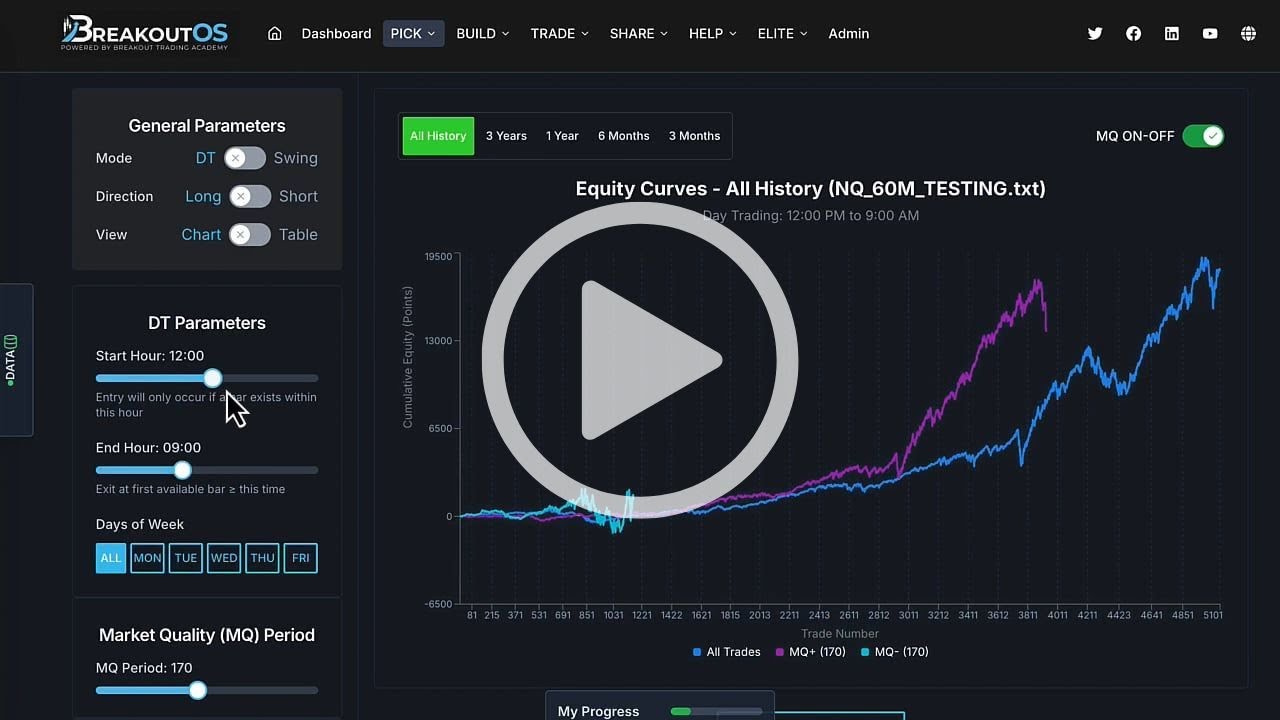

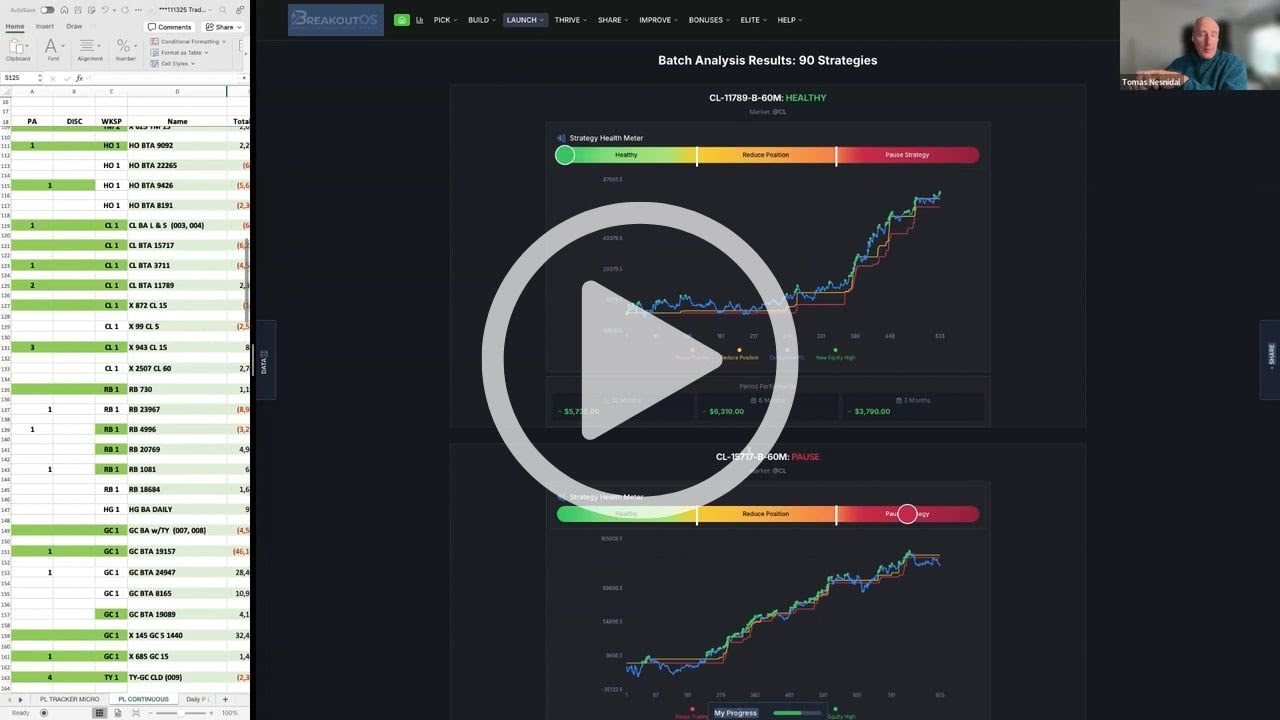

A BreakoutOS member running 90 strategies achieves 10% monthly profits using the Strategy Health Monitor's traffic-light system to rotate strategies weekly.

Read more →March 10, 2026

BreakoutOS members build and monitor breakout strategies with the Strategy Health Monitor. See real leaderboard results and portfolio-level performance.

Read more →March 6, 2026

ATR and volatility filters ranked first across 615 Bitcoin strategies while oscillators like RSI finished dead last. See the full BreakoutOS filter test results.

Read more →February 27, 2026

Bar range/ATR cut max drawdown 40% and boosted profit 60% across 3,500 NASDAQ strategies. See which filters work and which fail in BreakoutOS testing.

Read more →